Guides

Guides

FDI screening regimes in CEE & SEE

The 2025 Wolf Theiss guide – FDI screening regimes in CEE & SEE – offers a structured overview of foreign direct investment (FDI) screening regimes across Central, Eastern and Southeastern Europe (CEE & SEE). For each jurisdiction, the guide outlines the key requirements investors and advisors should be aware of – including which transactions and sectors are covered, whether filing is mandatory, which party is responsible for submitting the FDI notification, applicable deadlines and potential sanctions for non-compliance. Additional insights include whether filings are public, how long the review typically takes and whether exemptions apply. This guide is designed to support stakeholders navigating the region’s evolving regulatory landscape with clarity and confidence.

Download the full Guide

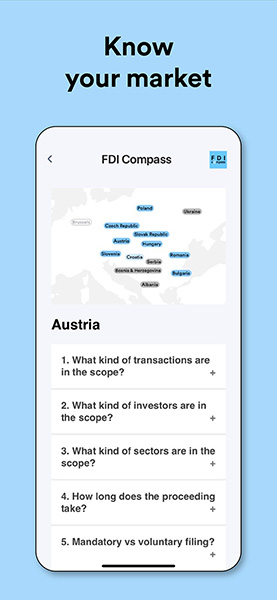

FDI Compass – your mobile FDI reference tool

FDI Compass provides a practical overview of foreign direct investment screening regimes across Central Eastern and South Eastern Europe. The app complements this guide with mobile-friendly access to the same jurisdictional content and is regularly updated.

Download the FDI Compass app:

Jurisdictional FDI screening regimes

The following chapters provide country-specific insights into the FDI screening regimes across our region. Each section highlights the applicable rules, procedures and practical considerations relevant to that jurisdiction.

Albania

Albania does not have an FDI screening regime.

Legislative process

At present, there is no effective national legislation in Albania implementing FDI control. As soon as an Albanian FDI screening regime has been adopted, this section will be updated.

Related experts

Austria

Austria’s FDI screening regime imposes strict regulations on foreign investments, particularly those made by non-EEA and non-Swiss entities. Investors acquiring voting rights or exerting decisive influence over Austrian businesses in critical sectors – such as defence, energy, telecommunications and cybersecurity – must comply with mandatory filing requirements. The process involves a multi-phase review, EU cooperation mechanisms and potential sanctions for non-compliance. While exemptions exist for micro-enterprises and certain intra-group transactions, businesses must navigate complex regulatory hurdles to ensure approval.

Download the chapter on Austria

Related experts

Bosnia & Herzegovina

Bosnia and Herzegovina does not have an FDI screening regime.

Legislative process

To date, there have been no legislative initiatives towards implementing a Bosnian FDI screening regime comparable to FDI regimes in EU Member States.

Bosnian non-EU comparable FDI screening regime

Foreign investment in the defence and media sectors need approval from the relevant authorities, pursuant to the Law on the Policy of Foreign Direct Investment.

Bulgaria

Bulgaria’s FDI screening regime requires approval for transactions involving non-EU investors (with certain exceptions) acquiring at least 10% of a company operating in Bulgaria or exceeding an investment threshold of EUR 2 million. The review process applies to key sectors such as critical infrastructure, cybersecurity, energy and high-tech industries, with heightened scrutiny for investors from Russia or Belarus. The approval procedure, managed by the Bulgarian Investment Agency and the FDI Council, should take approximately 60 days. Non-compliance may result in fines or investment restrictions.

Download the chapter on Bulgaria

Related experts

Croatia

Croatia has recently enacted legislation on FDI screening. The new framework entered into force on 13 November 2025, aligning national legislation with EU Regulation 2019/452 and ensuring consistency with European standards on security and public order. FDI screening captures acquisitions of 10% or more shares in a Croatian company by an acquiring entity established outside of EU/EEA, or where the acquiring entity is directly or indirectly controlled by an entity outside of EU/EEA.

Unfortunately, there is still little clarity on how wide the FDI screening obligations in Croatia will be cast. The new FDI legislation generally lists sectors which will be subject to screening (including energy sector, transportation, health sector, water and waste management, agriculture, technology, defence, media, digital infrastructure, banking and financial services); however, the implementing regulation to be adopted by the Government of Croatia within six months will set out specific activities within each of these sectors that will require FDI screening. Furthermore, based on this implementing regulation, specifically designated public authorities will individually name the entities that will be subject to screening. Our understanding is that only such specifically named entities will be subject to FDI screening process and that those entities that are not specifically named (even if they belong to one of the general sectors listed above) will be subject to screening. Accordingly, the prevailing view is that FDI screening cannot be effectively carried out until the relevant implementing regulations are in place.

The screening regime will apply retroactively. All qualifying foreign acquisitions, irrespective of when they occurred and without any limitation period, will be subject to screening.

Related experts

Czech Republic

The Czech FDI screening regime applies to foreign investors from outside the EU, including those from the UK, Switzerland and EEA countries. Investments in military production, critical infrastructure, dual-use goods and media require approval. Transactions granting at least 10% voting rights, control over assets or access to sensitive technology are subject to scrutiny. The process takes up to 135 days, with mandatory filings for high-risk sectors and voluntary consultations for others. Non-compliance can result in fines of up to 2% of annual turnover or forced divestment.

Download the chapter on the Czech Republic

Related experts

Hungary

Hungary operates two FDI screening regimes: the General Hungarian FDI screening regime (2019) and the Alternative Hungarian FDI screening regime (2020). Both require mandatory filings for foreign investments in strategic sectors, including energy, telecommunications, defence and financial services. Transactions reaching voting thresholds between 5 to 50% may require approval. The General regime applies to non-EU/EEA/Swiss investors, while the Alternative regime also covers certain EU-based investors. The review process takes up to 60 days under the General regime and 30 business days under the Alternative regime. Non-compliance may lead to fines or transaction nullification.

Download the chapter on Hungary

Related experts

Poland

Poland’s FDI screening regime applies to direct and indirect foreign investments in strategic companies and sectors, covering energy, telecommunications, defence and critical infrastructure. Transactions involving a Polish-registered company, a foreign investor (non-EU/EEA/OECD) and revenues exceeding EUR 10 million require approval. The screening process includes a 30-business-day preliminary review and, if necessary, a 120-day detailed investigation. Filing is mandatory and closing transactions before clearance is strictly prohibited. Non-compliance may result in nullified transactions, fines up to EUR 22 million or even imprisonment.

Download the chapter on Poland

Related experts

Romania

The Romanian FDI screening regime applies to non-EU investors and EU investors controlled by non-EU entities, covering direct, indirect and greenfield investments in strategic sectors such as critical infrastructure, energy, defence, telecommunications (including 5G) and media. Filing is mandatory for investments exceeding EUR 2 million and transactions cannot be implemented before clearance. The review process takes up to 135 days for non-EU investors and 70 days for EU investors, with an additional 90-day in-depth review in cases involving national security concerns. Non-compliance may lead to fines of up to 10% of the investor’s global turnover or even annulment of the transaction.

Download the chapter on Romania

Related experts

Serbia

Serbia does not have an FDI screening regime.

Legislative process

So far there have been no legislative initiatives towards implementing a Serbian FDI screening regime comparable to FDI regimes in EU Member States.

Serbian non-EU comparable FDI screening regime

Serbia operates a single-sector authorisation system covering the defence sector, specifically foreign investments in the production of arms and military equipment. The legislation regulating this authorisation system for the defence sector is the Law on Production and Trade of Arms and Military Equipment.

Slovak Republic

In Slovakia, the FDI screening process applies to acquisitions or increases in control over Slovak businesses, particularly in sensitive sectors such as critical infrastructure, defence and technology. Foreign investors, including natural persons from outside the EU and entities controlled by non-EU nationals, are subject to this regime. Transactions involving significant stakes or decision-making influence must undergo scrutiny to mitigate risks to public safety and national security. Filing is mandatory for investments in strategic sectors, while non-critical investments allow voluntary filing. Prior approval is required before closing and post-closing reporting obligations apply. Non-compliance may result in fines of up to 2% of global turnover or EUR 200,000 for administrative breaches.

Download the chapter on the Slovak Republic

Related experts

Slovenia

Slovenia’s FDI screening regime focuses on foreign investments that could potentially impact national security or public order. It applies to both EU and non-EU investors across a wide range of sectors, including critical infrastructure, defence and emerging technologies. Filling is mandatory for investments in these sectors but does not suspend closing. Investors must notify the Slovenian FDI authority within 15 days of certain significant transactions and the authority has the power to impose sanctions if the rules are not followed or if investments do not align with national interests. Failure to comply may result in fines of up to EUR 500,000 and prohibited transactions may be considered invalid as of their signing date.

Download the chapter on Slovenia

Related experts

Ukraine

Ukraine does not have an FDI screening regime.

However, investors should consider the potential need for merger clearance if their transactions meet the thresholds that trigger such a requirement. Additionally, in certain industries such as banking, insurance or media, investors should factor in a possible requirement to notify or obtain approval for their transactions from the respective industry regulators, provided the relevant criteria are met.

Finally, as a matter of practice, the Government of Ukraine involves the State Security Service (the national intelligence and counterintelligence agency) in major privatisation transactions for the purpose of screening successful bidders intending to acquire state-owned assets or companies.

Legislative process

At the end of September 2025, a draft law introducing an FDI screening regime in Ukraine (the “Draft Law”) was registered in the Parliament of Ukraine. The Draft Law aims not only to introduce an FDI screening regime into the Ukrainian investment framework, but also, from the outset, to align national legislation in this area with EU and US standards, as well as to reflect global trends in investment control.

The Draft Law is presently at its earliest stage of consideration by the relevant parliamentary committee and the Parliament of Ukraine. It is expected that the provisions of the Draft Law will be subject to changes during the process of its consideration.

Once adopted, the Draft Law will come into effect six months following its publication. Upon becoming effective, it will not affect investments and transactions closed prior to its entry into force.