The European Union’s Regulation (EU) 2023/1114 on Markets in Crypto-Assets (“MiCA“) became directly applicable on 30 December 2024. Bulgaria has now enacted its Law on the Markets in Crypto-Assets (the “Bulgarian MICAL“), giving the country full implementation of MiCA and triggering immediate obligations for crypto-asset issuers and service-providers.

EU regulatory background

MiCA introduces a single passportable licence for crypto-asset service providers (“CASPs”), imposing uniform conduct-of-business rules and prudential requirements, tiered by service class (the higher of EUR 50 000, EUR 125 000 or EUR 150 000 in paid-in capital or one quarter of the fixed overheads of the preceding year, reviewed annually). Article 143(3) of the MiCA allows Member States to reduce or waive the default 18-month grandfathering period (30 December 2024–1 July 2026) for entities that were already providing crypto-asset services under pre-existing national law.

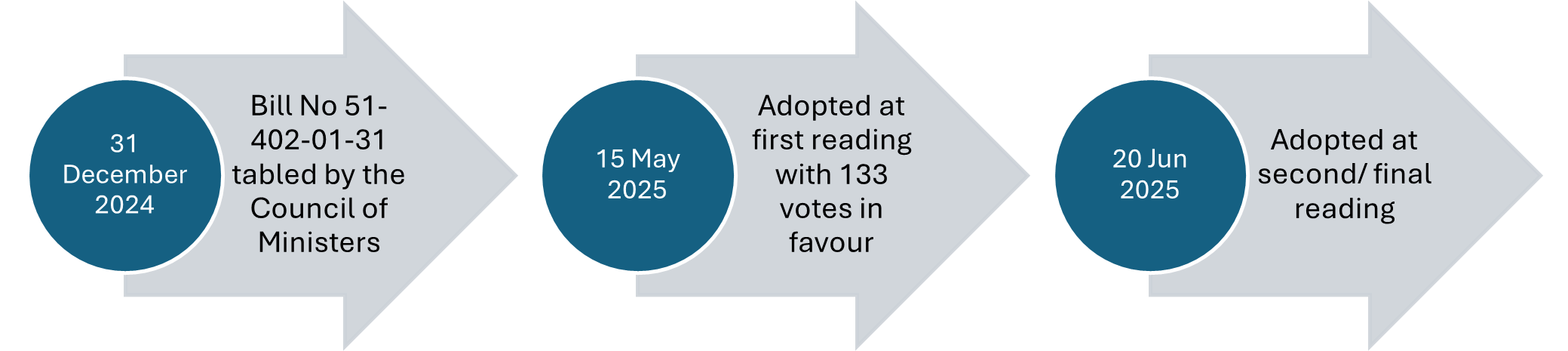

Implementation of MiCA in Bulgaria Bulgaria has opted for the full 18-month grandfathering period (until 1 July 2026), while attaching strict fit-and-proper and organisational tests to all applicants. Below is the legislative timeline for the enactment of the Bulgarian MICAL, pending its publication in the State Gazette:

Key features of the Bulgarian MICAL

- Token taxonomy clarified. The Bulgarian MICAL tracks MiCA’s three-pillar classification of crypto-assets: (i) asset-referenced tokens (“ARTs“), (ii) electronic money tokens (“EMTs“) and (iii) “other” crypto-assets.1 Distinct prudential and disclosure rules now attach to each pillar, ending years of doctrinal ambiguity in Bulgarian law.

- Supervisors. The Financial Supervision Commission (“FSC“) is the default competent authority for MiCA in Bulgaria. It licences and monitors asset-referenced-token issuers and CASPs.2 Where MiCA vests powers in the prudential supervisor of electronic-money tokens, those powers fall to the Bulgarian National Bank (“BNB“). The Bulgarian MICAL expressly carves EMT issuers out of the Act (save for market abuse rules in MiCA Title VI).3 EMT issuers must therefore be authorised under the Bulgarian Payment Services and Payment Systems Act (the “Bulgarian PSPSA“), for which the BNB is the licensing and supervisory body4. MiCA itself confirms that, as the EMT issuer is required to be an electronic money institution or a credit institution, the same prudential supervisor continues to be the competent authority for MiCA purposes5. The two regulators must cooperate: the FSC coordinates with ESMA and EBA6 and must notify the BNB when it applies certain enforcement measures to a credit-institution EMT issuer.7

- Licence timeline. The FSC must issue or refuse a CASP licence or an asset-referenced token licence within the terms envisaged under MiCA. The initial Bill envisaged that failure to reply would be deemed a refusal (“silent denial”). However, between first and second reading, the MPs scrapped the rule that the FSC inaction equals to silent denial. Commentators hail this as a “major predictability upgrade for investors”.8 The supervisor must now issue an express, reasoned decision within the timeframes envisaged under MiCA.9

- Transitional regime. Any virtual-asset service providers (“VASPs“) recorded in the National Revenue Agency AML register before 30 Dec 2024 may continue, without a licence, to carry out in the territory of the Republic of Bulgaria the activity for which they are registered until 1 July 2026 or until they obtain (or are refused) a MiCA licence, whichever is earlier.10 VASPs recorded in the National Revenue Agency AML register between 30 December 2024 and the date on which the Bulgarian MICAL enters into force are required to file an application for a MiCA licence within three months of that entry into force. Within thesame period, those persons are required to bring their activities into compliance with the MiCA and the Bulgarian MICAL.11

- Sanctions. Sanctions are envisaged in the MiCA itself and implemented in the Bulgarian MICAL. Administrative fines may reach the higher of BGN 5 million or 6.25 % of global annual turnover for a first offence and up to the higher of BGN 10 million or 12.5 % for a repeat breach. For certain specified breaches, the fine may be the higher of BGN 15 million or 7.5 % of global annual turnover for a first offence and up to the higher of BGN 30 million or 15 % for a repeat breach.12 In addition, the FSC is empowered to:

-order an immediate suspension of a crypto-asset service for up to 30 working days or impose a permanent ban;13

-halt or prohibit a public offer or the trading of certain crypto-assets on a platform;14

-compel issuers or CASPs to amend or withdraw white-papers and marketing materials that are incomplete or misleading;15

-dismiss individual board members or senior managers responsible for violations;16

-publish every enforcement measure and penalty on its website, thereby “naming and shaming” non-compliant firms.17

The FSC is authorised, “when no other effective means exist to halt the breach” of MiCA, to instruct any third party (e.g. hosting company, domain registrar, content-delivery network) to: (i) remove specific content; (ii) restrict access to an “online interface”18 (the website or app through which a CASP serves EU clients); or (iii) display an explicit warning to users landing on that interface. This measure is conditional on a risk of “serious harm to the interests of clients or crypto-asset holders” and may be complemented by a court-ordered injunction19. Opponents argue that these powers grant the FSC an Internet “kill switch’ and constitute a form of censure. Supporters, however, counter that the clause simply transposes Art.94(1)(aa) of MiCA, which gives national authorities identical powers to act against rogue cross-border operators. With the Bulgarian MICAL in force, Bulgaria shifts from draft proposals to a fully operational MiCA regime. Pre-registered VASPs have a narrow, domestic-only runway until 1 July 2026; all newcomers must prepare complete MiCA files and apply for a MiCA licence. The steep, turnover-based fines underscore the need for rigorous compliance from day one.

Download the Client Alert here

- Art. 5 of the Bulgarian MICAL. ↩︎

- Art. 3(1) of the Bulgarian MICAL. ↩︎

- Art. 1(2) of the Bulgarian MICAL. ↩︎

- To this effect, new Chapters 10a and 10b are introduced in the Bulgarian PSPSA with the Bulgarian MICAL. ↩︎

- Art. 48(1) of the MiCA. ↩︎

- Art. 3(2) of the Bulgarian MICAL and art. 96 of the MiCA. ↩︎

- Art. 22(1) of the Bulgarian MICAL. ↩︎

- https://forbesbulgaria.com/2025/06/20/okonchatelno-balgariya-ima-zakon-za-targoviyata-s-kriptoaktivi/ ↩︎

- Arts 6(2) and 15(5) of the Bulgarian MICAL. Under Art. 63(9) of the MiCA, competent authorities are required, within 40 working days from the date of receipt of a complete application, to assess whether the applicant crypto-asset service provider complies with the Act and to adopt a fully reasoned decision granting or refusing an authorisation as a CASP. Competent authorities are required to notify the applicant of their decision within five working days of the date of that decision. That assessment takes into account the nature, scale and complexity of the crypto-asset services that the applicant CASP intends to provide. ↩︎

- § 3(1) of the Transitional and Final Provisions of the Bulgarian MICAL. ↩︎

- § 3(2) of the Transitional and Final Provisions of the Bulgarian MICAL. ↩︎

- Arts 37(3) and 38(3) of the Bulgarian MICAL. ↩︎

- Art. 28(1), p.1-3, 5 of the Bulgarian MICAL. ↩︎

- Art. 28(1), p.10-13 of the Bulgarian MICAL. ↩︎

- Art. 28(1), p.7-9, 15 of the Bulgarian MICAL. ↩︎

- Art. 28(1), p.19 of the Bulgarian MICAL. ↩︎

- Art. 46(1) of the Bulgarian MICAL. ↩︎

- Art. 28(1), p. 27 of the Bulgarian MICAL. Definition of “online interface” is contained in § 1, item 9 (mirroring MiCA Art. 3(1)(38)) of the Bulgarian MICAL. ↩︎

- Under Art. 36 of the Bulgarian MICAL. ↩︎

Markets in Crypto-Assets (MiCA) licensing in Bulgaria

The European Union’s Regulation (EU) 2023/1114 on Markets in Crypto-Assets (“MiCA“) became directly applicable on 30 December 2024. Bulgaria has now enacted its Law on the Markets in Crypto-Assets (the “Bulgarian MICAL“), giving the country full implementation of MiCA and triggering immediate obligations for crypto-asset issuers and service-providers. EU regulatory background MiCA introduces a single […]...

Wolf Theiss advises AURELIUS on the acquisition of Winkelmann Automotive Poland (WAP), a subsidiary of Winkelmann Group

Warsaw, 26 June 2025 – Wolf Theiss advised AURELIUS, a globally active alternative investor focused on private equity, private debt and real estate, on the acquisition of Winkelmann Automotive Poland, a renowned manufacturer of torsional vibration dampers based in Poland. The acquisition complements AURELIUS’ purchase of MUVIQ in 2024 – a global automotive supplier that […]...

Wolf Theiss advises New Wave Group on the acquisition of Cotton Classics Handels GmbH

Prague, 26 June 2025 – Wolf Theiss advised New Wave Group AB, a Swedish growth company that designs, acquires and develops brands and products in the corporate promo, gifts and home furnishings sectors, on the acquisition of 100% of the shares in Austrian textile wholesaler Cotton Classics Handels GmbH. The Wolf Theiss team, working alongside […]...

Tightening the grip – Hungary introduces updates to its foreign investment screening processes

Hungary’s specific domestic foreign direct investment (FDI) screening regime (affecting both ongoing and future cases) has been updated to include extended applicable deadlines and the possibility of multiple rounds of extensions. Additionally, the existing pre-emption mechanism – originally intended for transactions targeting solar developments – has been extended to cover all transactions blocked by the […]...

Wolf Theiss advised CWR Realitäten GmbH on the sale of the voco Vienna Prater hotel

Vienna, 25 June 2025 – Ahead of upcoming changes to the real estate transfer tax on share deals, the shares in Engerth 173-175 Entwicklungs GmbH & Co KG – the property owner and lessor of the voco Vienna Prater hotel – were sold to Nowu Hospitality GmbH. Formerly operated as Austria Trend Hotel Lassalle, the […]...

Verwaltungsgerichtshof zur grenzüberschreitenden Arbeitskräfteüberlassung

In dieser Folge des Arbeitsrechts-Podcasts von Wolf Theiss erörtern Hemma Elsner und Matthias Unterrieder eine aktuelle Entscheidung des Österreichischen Verwaltungsgerichtshofs (VwGH Ro 2024/11/0002) zur grenzüberschreitenden Arbeitskräfteüberlassung. Gegenstand war die Frage, ob die Überlassung von Arbeitskräften an ein Unternehmen mit Sitz in einem Drittstaat auch dann eine genehmigungspflichtige grenzüberschreitende Überlassung sein kann, wenn die Arbeitskräfte physisch […]...

Chambers Acquisition Finance 2025 Guide: Slovenia

Wolf Theiss lawyers Markus Bruckmüller, Klemen Radosavljević and Matej Kraner have authored the chapter on Slovenia in the Acquisition Finance 2025 Guide, published by Chambers and Partners, offering insight into the evolving legal framework, deal structures, lender behavior and cross-border financing. In Slovenia, the acquisition finance market is supported by a strong banking sector comprising […]...

EU schließt chinesische Unternehmen von Großaufträgen im Medizinprodukte-Sektor aus

Erste Maßnahme nach dem IPI-Instrument und weiterer Schritt im härter werdenden Vorgehen gegen China Mit der am Freitag, 20. Juni 2025, veröffentlichten Durchführungsverordnung (EU) 2025/1197 beschloss die Europäische Kommission, Unternehmen aus der VR China von öffentlichen Aufträgen für Medizinprodukte auszuschließen. Betroffen sind Aufträge mit einem geschätzten Auftragswert von mehr als fünf Millionen Euro. Weiters dürfen […]...

Wolf Theiss advises Sekyra Group on the sale of an affordable housing project in Prague

Prague, 18 June 2025 – The Wolf Theiss real estate team assisted Sekyra Group with closing the sale of the residential project Opatov II – comprising 307 rental apartments – to Dostupné bydlení České spořitelny, a.s. (a part of Erste Group AG) and Kooperativa pojišťovna, a.s. (a part of Vienna Insurance Group AG). The Wolf […]...

Fristen im Vergaberecht

In dieser Folge unseres Vergaberecht-Podcasts diskutieren Manfred Essletzbichler und Johann Hwezda das Thema “Fristen im Vergaberecht”, ein oft unterschätzter, aber entscheidender Aspekt jedes Vergabeverfahrens. Unsere Vergabeexperten erörtern die zentralen Fristvorgaben des BVergG – von Angebots- und Teilnahmefristen über Rechtsschutzfristen bis hin zu Sonderregelungen für beschleunigte Verfahren. Sie erklären, was unter einer “angemessenen” Frist zu verstehen […]...

Neuer Rechtsrahmen zur digitalen Barrierefreiheit ab 28. Juni 2025

Das Barrierefreiheitsgesetz (BaFG) verpflichtet Unternehmen zur barrierefreien Gestaltung digitaler Produkte und Dienstleistungen Am 28. Juni 2025 tritt das BaFG (BGBl I 76/2023) in Kraft. Es setzt die Richtlinie (EU) 2019/882 über die Barrierefreiheitsanforderungen für Produkte und Dienstleistungen (European Accessibility Act – EAA) in nationales Recht um und bringt bedeutende Änderungen für zahlreiche Unternehmen in Österreich […]...

M&A in the defence sector

Select key considerations for strategic and financial buyers Heightened geopolitical tensions, NATO rearmament drives and persistent threats to European security have pushed the defence sector to the top of many investors’ agendas. With governments across Europe recommitting to hard power, defence M&A is entering a phase of strategic relevance not seen since the Cold War. Yet, […]...